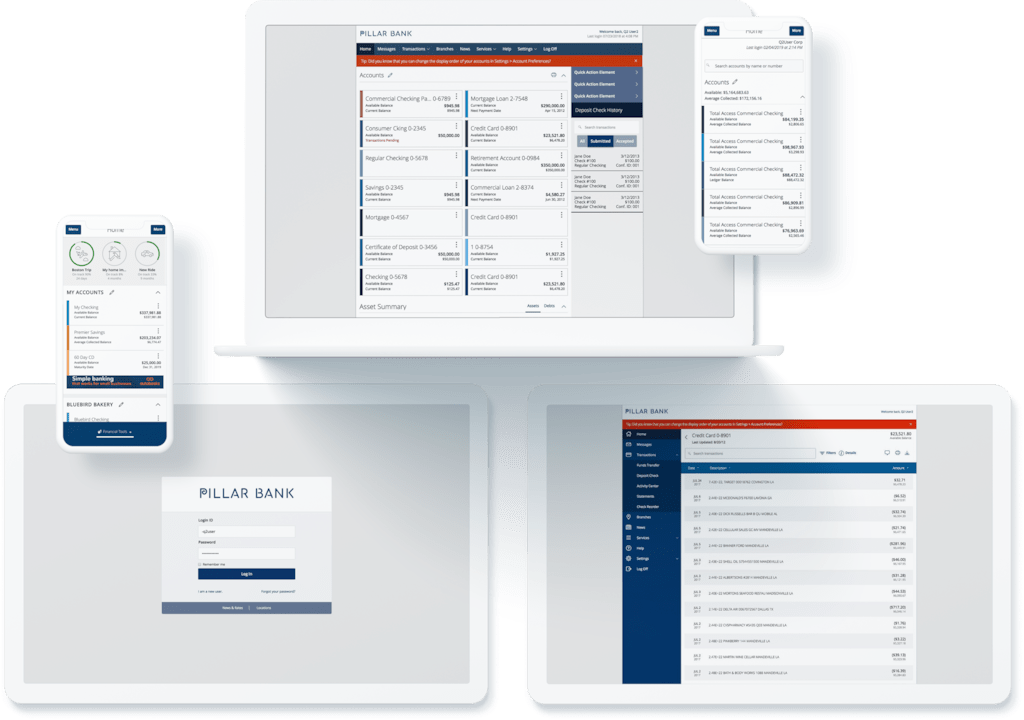

What’s next in commercial banking

Introducing Q2 Catalyst: an extensive, holistic digital solution for commercial banking. Win more, onboard faster, serve better, and grow stronger relationships. With treasury management tools, small business solutions, relationship pricing, a fintech marketplace, and more, Q2 Catalyst is a growth engine for your business and your community.

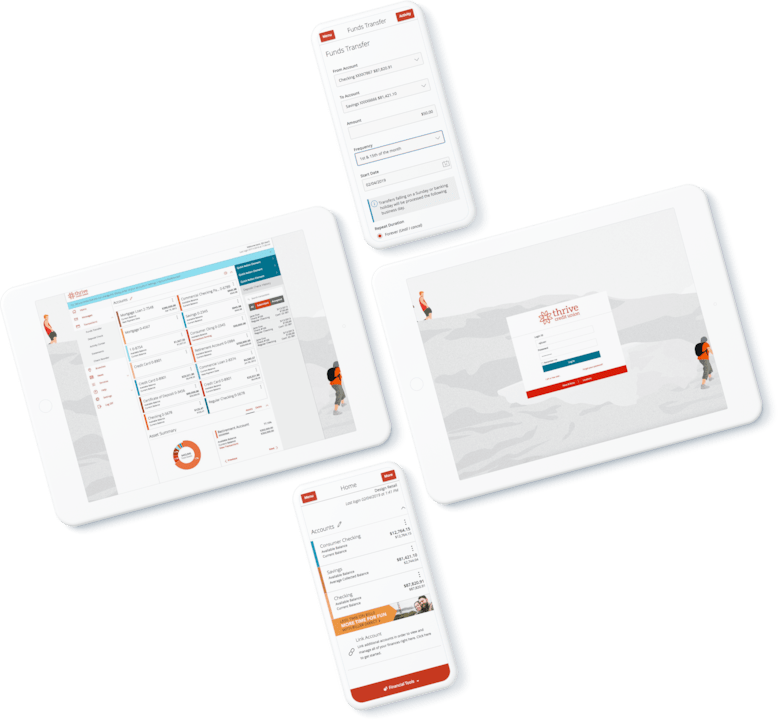

Consumers are looking for more than just checking accounts or debit cards.

They’re looking for quick, intuitive account opening, easy online borrowing, seamless security, and financial wellness tools and advice—including new ways to save, send money, and make purchases.

It’s your legacy that matters.

Legacy financial technology has blocked innovation for too long. The market is hungry for new solutions, pricing structures, and experiences.

>20M Users

The Q2 digital banking platform serves over 20 million end users.

>1.5B Saved

In 2021, Q2 prevented over 1.5 billion in business banking check fraud.

>1M Onboarded

We onboarded over a million new financial accounts last year.

>150% Growth

We’ve improved our customers’ digital marketing success rates by over 150%.

Customer Stories

Browse All →-

Generations Federal Credit Union partners with Q2 to attract younger members

Membership of younger population grew and overall membership increased

-

Q2 helps Amplify Credit Union go fee-free

Grew checking accounts 5% faster and savings accounts 9% faster

-

FAIRWINDS Credit Union improves member experience with Q2

216% increase in ACH transactions

-

Tri Counties Bank increases online account openings with Q2

Online account openings increased by 75%